Contents

Mill AI Research | Published: April 2026

---

Executive Summary

Poland ranks second-to-last in the European Union for AI adoption in business, with 8.4% of companies using AI against an EU27 average of 20.0%. That number tells only part of the story. Eurostat surveys only firms with 10 or more employees, which means official statistics omit 95.9% of Poland's business registry, roughly 2.76 million small businesses and solopreneurs who constitute the backbone of the Polish small-business economy. This is the first report to map that blind spot and examine what's happening with AI adoption where Eurostat doesn't reach.

Key findings:

- Eurostat measures 4.1% of Polish firms. The remaining 95.9% (about 2.76 million enterprises in the 0-9 employee bracket) sit outside official AI adoption surveys. 82.4% of new business registrations in Q1 2025 were sole proprietorships, a segment about which systematic data on AI is virtually nonexistent.

- The gap is widening, not closing. Poland grew from 5.9% to 8.4% between 2024 and 2025 (+2.5 pp), while the EU27 jumped from 13.5% to 20.0% (+6.5 pp). Denmark accelerated by 14.5 pp in a single year, five times faster than Poland.

- Content = use case number one, globally and locally. 55% of marketers (HubSpot) cite content creation as the top AI use case; 34.08% of EU27 AI-using firms deploy it in marketing and sales. In Poland, marketing and sales is also the leading use case, 5.0% of all firms.

- The language penalty is real and measurable. The best AI models score 83% on the PLCC benchmark (Polish Linguistic & Cultural Competency), while the same models achieve 90%+ on English MMLU. Implied penalty: 7-10 percentage points on Polish.

- AI-using firms grow faster. 66% of Polish AI adopters expect revenue growth within 3 years, 20+ pp more than non-adopters (PIE). Global data from Salesforce SMB Trends shows 91% of small firms using AI report revenue growth and 87% scale faster.

The report synthesizes data from Eurostat, GUS (Polish Central Statistical Office), PIE (Polish Economic Institute), KPMG, HubSpot, Salesforce, and academic benchmarks of language-model quality in Polish.

---

Methodology

This report synthesizes data from eight independent sources published between January 2025 and February 2026. The goal was to reconstruct the fullest possible picture of AI adoption in Poland's enterprise ecosystem, with particular focus on the segment that official European statistics consistently omit.

Primary sources (adoption statistics): Eurostat ICT Usage in Enterprises module, editions 2021, 2023, 2024, and 2025 (published January 2025 and January 2026). The survey covers firms with 10 or more employees in non-financial sectors, excluding agriculture, fishing, and public administration. The 10+ threshold is a deliberate design choice to preserve international comparability and time-series stability, not a methodological oversight. Our observation is not that Eurostat counts wrong, but that in the Polish context the 10+ threshold excludes 95.9% of the firm registry, while in Western economies (with higher average employment per firm) the same threshold excludes far less. GUS data for 2025 (December 2025 release, cited by biznes.pap.pl) shows 8.7% for Poland, marginally higher than Eurostat's 8.4% due to differences in the exact sample.

Secondary sources (firm structure): GUS, REGON, and active business entities Q3 2025. This dataset allows estimation of the real scale of the segment Eurostat omits.

Industry sources (use cases): HubSpot State of Marketing 2025/2026 (n = 1200+ global marketers), Salesforce SMB AI Trends 2025 (n = 3350 SMB owners), Polish Economic Institute (Digital Transformation Monitor 2025), KPMG Digital Transformation Monitor 2025 (n = 180 mid-size and large firms in Poland).

Academic sources (AI quality in Polish): PLCC benchmark (Polish Linguistic and Cultural Competency), published as arXiv preprint 2503.00995, measuring the performance of twelve language models, both commercial and open-source, on tasks requiring comprehension of Polish linguistic and cultural context.

Limitations. The most important limitation is that none of the major sources systematically measures AI adoption in firms of the 1-9 employee bracket or among sole proprietorships. Where we discuss that segment, we rely on extrapolations and industry data that includes solopreneurs (HubSpot Solopreneur Report, Salesforce SMB Trends both sample below the Eurostat employment threshold).

All numbers were confirmed in at least two independent sources where possible. Where discrepancies exist (e.g., Eurostat 8.4% vs GUS 8.7%), both values are shown.

---

Finding 1: The Eurostat Blind Spot

When Eurostat published its annual EU AI adoption report on January 23, 2025, headlines across Polish media converged: Poland second-to-last, only 5.9% of firms using artificial intelligence. A year later, in January 2026, the picture improved slightly to 8.4%, but Poland still ranked second from bottom, ahead only of Romania (5.2%) and level with Bulgaria (8.5%).

The numbers are accurate. They are also misleadingly incomplete.

Eurostat's methodology was inherited from the 1990s, when the shared European ICT statistics system was built, and covers firms with 10 or more employees. On paper this is reasonable: smaller firms are harder to sample, less stable over time, and their technology behavior was historically considered derivative of larger entities' decisions. In the Polish context it means Eurostat surveys a narrow slice of the economy.

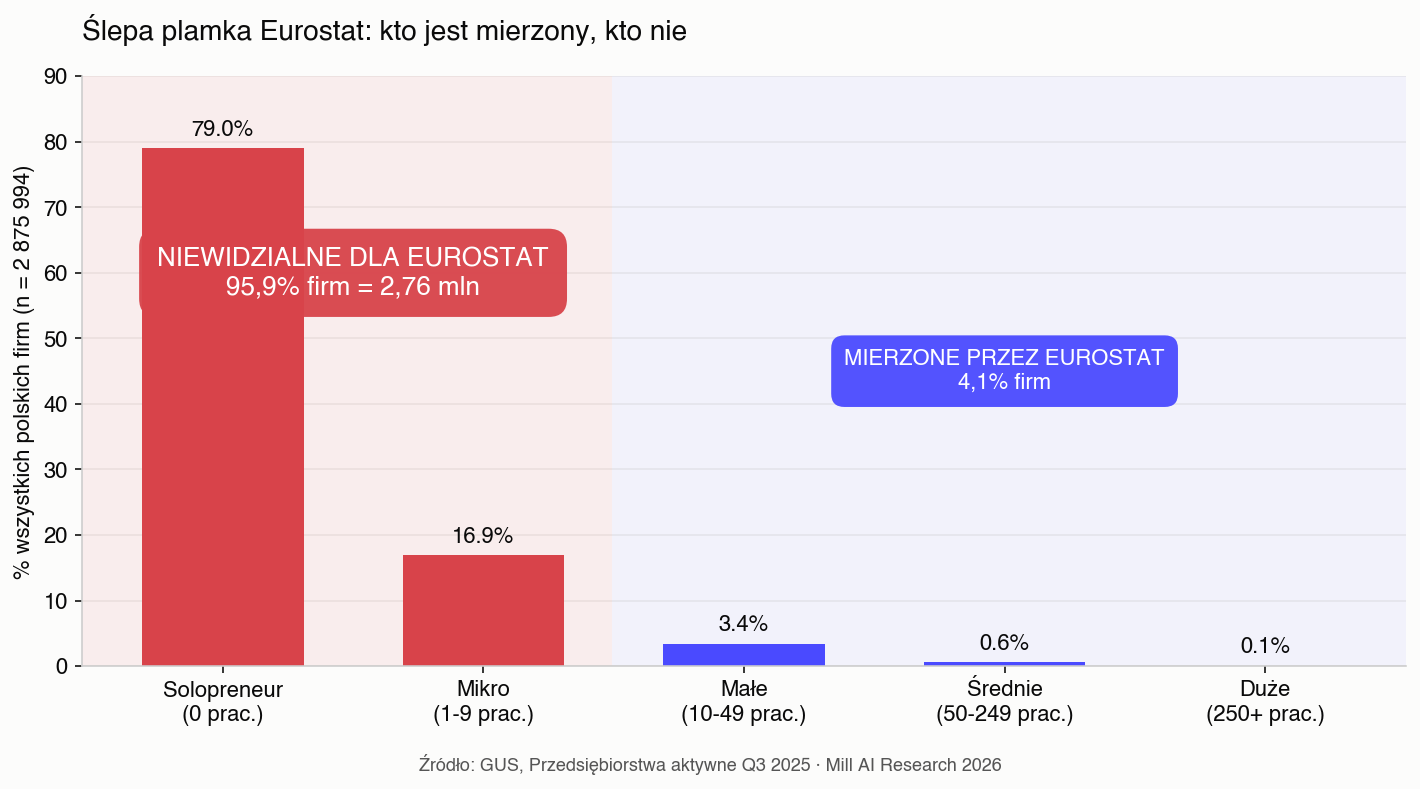

According to GUS, in Q3 2025 Poland had 2,875,994 active business entities. Of these:

- Firms with 0-9 employees: 95.9%, roughly 2.76 million

- Small (10-49): 3.4%

- Medium (50-249): 0.6%

- Large (250+): 0.1%

When we hear '8.4% of Polish firms use AI', we are talking about 8.4% of the 4.1% of firms registered in Poland. The remaining 95.9% (solopreneurs, small-business owners, freelancers on sole proprietorship, family businesses, boutique e-commerce) are invisible to official statistics.

The segment Eurostat omits is precisely the segment where most of the dynamism in the Polish economy is happening. In Q1 2025, sole proprietorships accounted for 82.4% of new business registrations (GUS) - flow, not stock (JDG share in the active registry is ~78-80%). Owners of marketing agencies, legal practices, photography studios, online shops, and accounting offices, even if their businesses thrive for the next decade, will never show up in Eurostat data because the methodology simply doesn't cover them.

'Eurostat measures 4.1% of Polish firms. The remaining 95.9%, roughly 2.76 million enterprises, sit outside official AI adoption statistics.'

Politically this matters because budget decisions, support programs, and digital strategies in ministries are anchored in Eurostat data. When sector plans read 'only 8.4% of Polish firms use AI, so we need an SMB support program', that program is designed for 4.1% of the firm population, not for the 95.9% that actually constitute the bulk of small business. The result: grants reach those already on the adoption path, rather than those who could yet enter it.

Commercially it matters because the market for AI tools designed natively for the Polish solopreneur is narrow. Global providers (OpenAI, Anthropic, Google) design for enterprise or English-speaking freelancers. Poland has a mature AI-native ecosystem (Brand24, Tidio, LiveChat, Edrone, Synerise, Autenti), but it targets mid-market and enterprise where budgets are legible. The layer of tools for the 1-3 person micro-firm operating in PLN and Polish-only remains fragmented. The 2.76 million small firms nobody systematically measures is also the segment nobody systematically builds for.

---

Finding 2: Content Is Use Case Number One

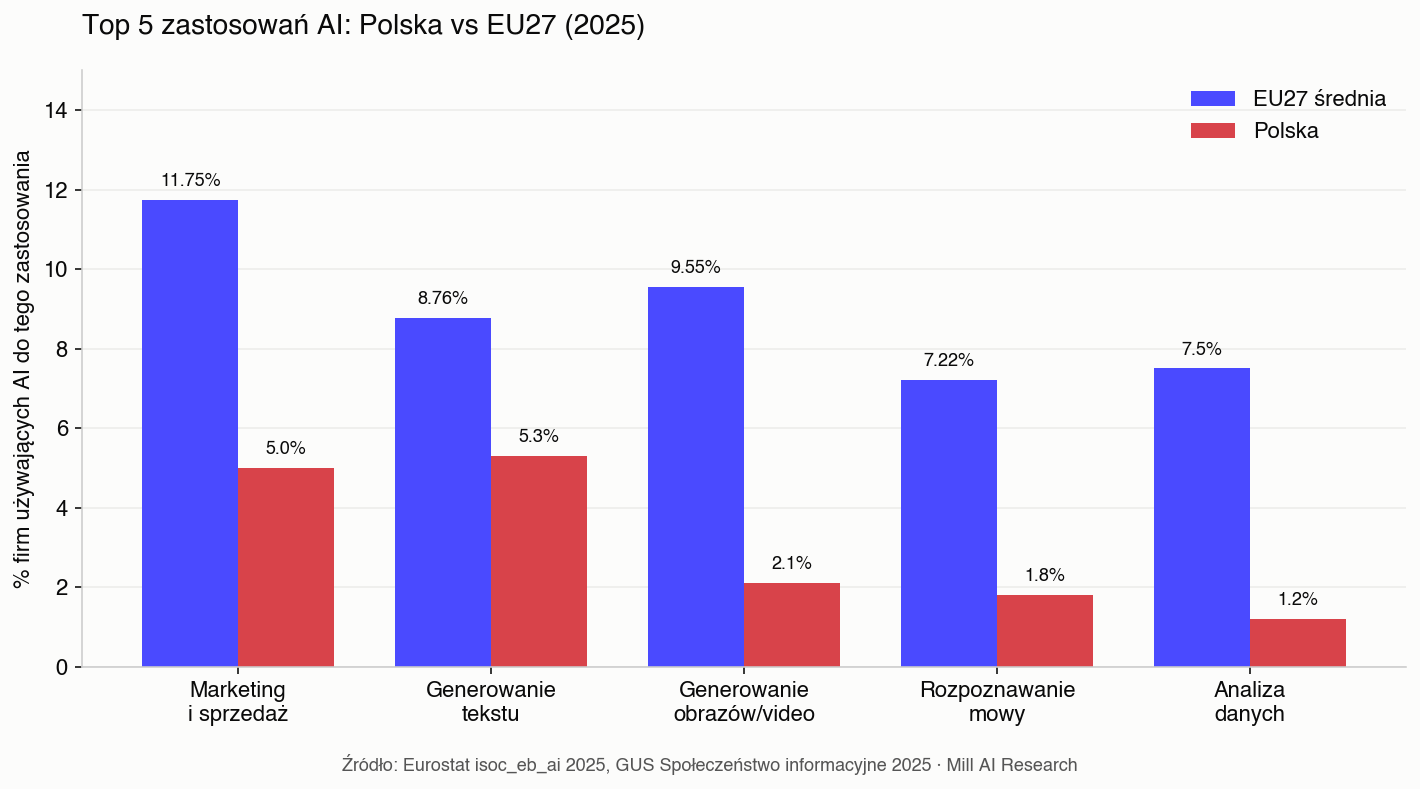

Across the EU27, the most common AI application in firms using the technology is marketing and sales, 34.08% of all AI users in 2024 (Eurostat). Administration and accounting comes second at 27.51%. The pattern is global and consistent: when firms start using AI, they start with content.

HubSpot State of Marketing 2025/2026 confirms this from the marketer's perspective: 55% of respondents cite content creation as the top AI use case in their organization. 94% plan to use AI for content in 2026. The detailed breakdown shows 46% use AI for copy, 47% for emails and newsletters, 46% for social posts, 38% for blogs, 56% for short-form video, 53% for images, 42% for long-form video. 86% of marketers say they carefully review and edit AI-generated content, which undermines the narrative that AI is replacing human copywriting. It isn't replacing it, it's moving the starting point.

Poland confirms the global pattern at smaller scale. According to GUS, in 2025 5.0% of all Polish firms use AI for marketing and sales, and this is the most common use case. 0.8% use AI in logistics (last place). Generative AI for text and voice generation is deployed by 5.3% of Polish firms overall, but in the Information & Communication sector the figure jumps to 25.5%. In construction it drops to 2.6%.

Marketing and sales win as use case #1 for three converging reasons at once: output is immediately verifiable (copy either sells or it doesn't, no six-month wait for data), pressure on volume against limited resources is greatest (every firm needs more content than it can produce), and the implementation barrier is minimal (no integration needed, no developer, no compliance check, just an account in an AI tool and an idea for the first prompt).

The implication for the Polish small-firm segment is straightforward. If the biggest AI use case is content, and the biggest market gap in Poland concerns solopreneurs and small firms, the question isn't 'do these firms need AI' but 'are they served today by tools that understand their context'. A Polish freelancer launching a marketing agency needs to write pitches in Polish, to Polish clients, in language that doesn't read like Google Translate. ChatGPT can handle it, but not without user intervention, iteration, and the risk of early disappointment with quality.

---

Finding 3: The Language Penalty

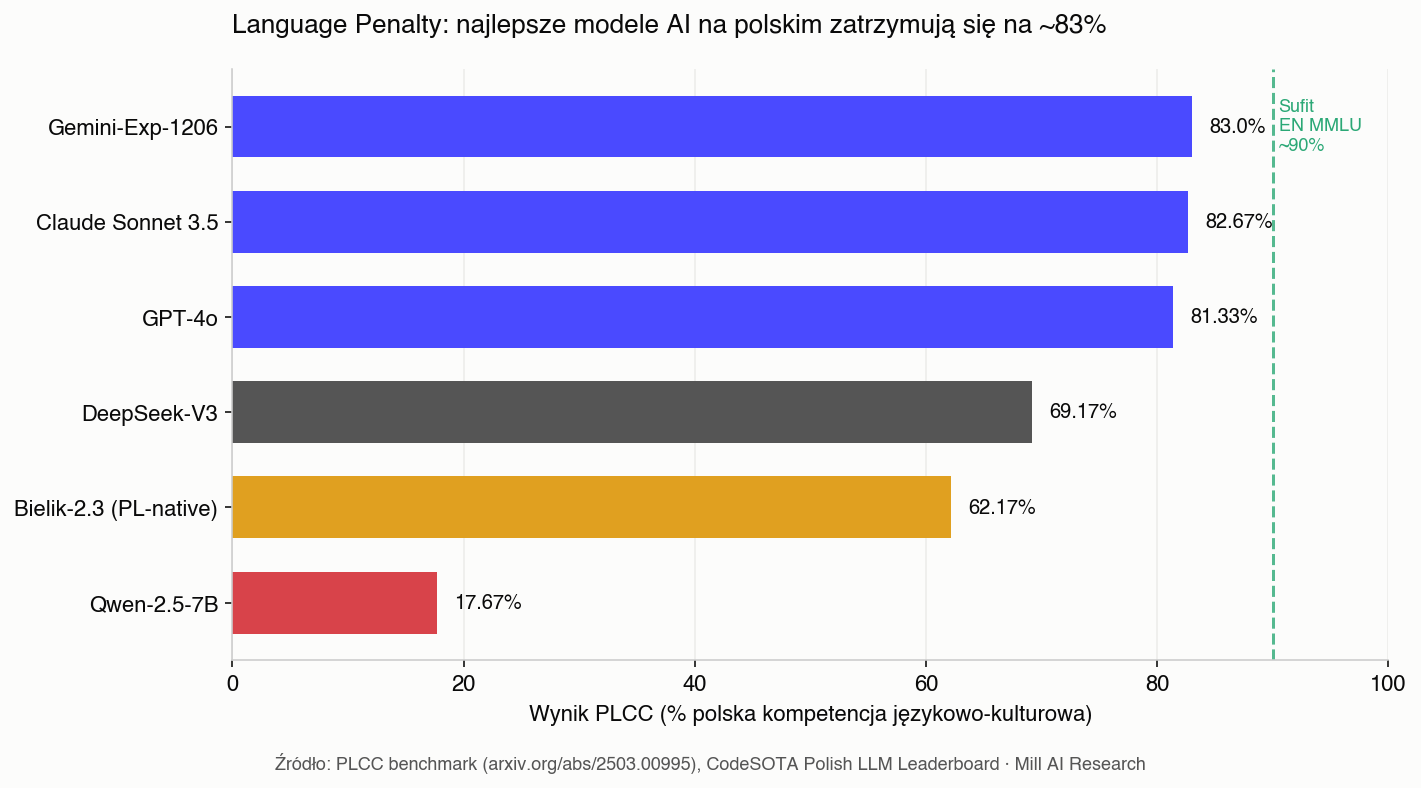

There is no globally accepted benchmark for 'AI quality in Polish'. The closest available is PLCC (Polish Linguistic and Cultural Competency), published as arXiv preprint 2503.00995. The benchmark tests language models on tasks involving Polish cultural contexts - idioms, historical references, register nuances - beyond plain translation.

Top model results:

- Gemini-Exp-1206 (Google): 83.00%

- Claude Sonnet 3.5 (Anthropic): 82.67%

- GPT-4o (OpenAI): 81.33%

- DeepSeek-V3: 69.17%

- Bielik-2.3 (Polish-native open-source, 11B parameters): 62.17%

- Qwen-2.5-7B: 17.67%

The same models achieve 90%+ on English MMLU (the common English-language benchmark), but the PLCC to MMLU comparison is not apples-to-apples: PLCC tests Polish linguistic and cultural competency, MMLU measures general academic knowledge in English. What the juxtaposition yields is a signal, not a hard number: the quality ceiling for AI in Polish is noticeably lower than in English. Conservative estimates of the gap - based on the PLCC authors' own writeup and two-step comparisons (translation, generation, native-speaker evaluation) - range from 5 to 12 pp, depending on task and model.

The authors of 2503.00995 write plainly:

"For multilingual abilities, particularly understanding cultural and linguistic context, open models are still significantly behind those offered as a service."

For a Polish marketer using ChatGPT to write a LinkedIn post, the penalty means a higher percentage of generated content that reads stiffly, mechanically, or requires a second editorial pass. For a Polish e-commerce owner using AI for product descriptions, it means the model sometimes picks the wrong register, too formal, too academic, unsuited to the Polish customer. For a Polish law firm, it means AI may mistranslate an Anglo-Saxon legal term whose Polish counterpart has different meaning.

The language penalty is not theoretical, it is measurable, repeatable, and has direct impact on adoption. A Polish SMB that tries ChatGPT and in the first five outputs gets material requiring heavy rework draws a conclusion: 'this doesn't work for Polish'. The conclusion is simultaneously true (for default settings) and false (because with proper prompting, model choice, and fine-tuning it works well), except that not every solopreneur has time to learn prompting.

What this produces is a market gap that functions as both an adoption constraint and a business opportunity, room for natively Polish tools.

---

Finding 4: The Gap Is Widening

The common assumption that Poland will 'catch up' to the European average within a few years is not supported by the data. The opposite is true: in each successive year, the gap between Poland and the EU27 grows, not shrinks.

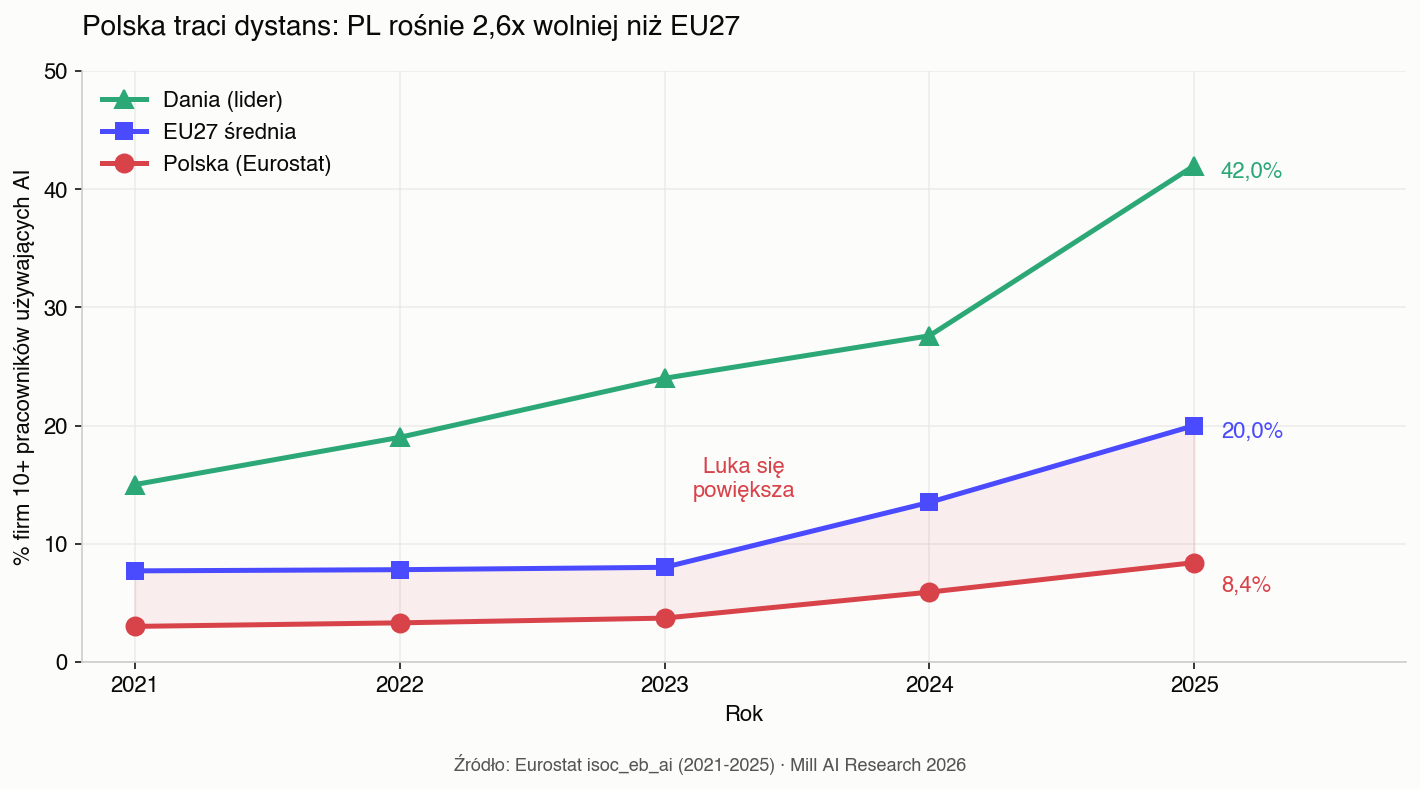

Poland 2021: approximately 3%. 2023: 3.7%. 2024: 5.9%. 2025: 8.4%.

EU27 2021: 7.7%. 2023: 8.0%. 2024: 13.5%. 2025: 20.0%.

In 2021 the gap was 4.7 pp. In 2025 it reached 11.6 pp. The gap grows year over year.

The 2024->2025 year shows the dynamic most sharply. Poland added +2.5 pp. The EU27 added +6.5 pp, 2.6 times faster. Leaders grew faster still. Denmark went from 27.6% (2024) to 42.0% (2025), +14.5 pp in a single year, five times faster than Poland. Finland at 37.8%, Sweden at 35.0%.

What drives the difference? Several factors compound.

Sectoral structure. Nordic countries have proportionally larger shares of AI-sensitive sectors (technology, professional services, finance). Poland has proportionally more industry, agriculture, and construction, sectors where AI adoption is slower (construction in PL: 2.6%).

Language. Danish, Finnish, and Swedish have stronger support in commercial models relative to their population size because those markets are wealthier and earlier shaped the roadmaps of OpenAI and Google. Polish, despite 38 million users, holds a weaker commercial position in the eyes of global providers.

Firm structure. Large firms adopt AI many times faster than small ones. In Poland, large firms are 0.1% of the registry. In the EU27 (average), large firms are also a small percentage, but their relative weight in adoption is larger because small firms in the EU are on average more technologically mature than Polish ones.

Adoption pipeline. Among Polish firms that do not yet use AI, only 3.9% say they are considering deployment in 2025 (GUS). The remaining 96.1% have no plans. 77% are decidedly opposed or neutral (PIE). A significant share of Polish entrepreneurs simply do not consider AI relevant to their business.

'Poland grows 2.6 times slower than the EU average and five times slower than Denmark. The 2025 gap is 11.6 pp and expanding year over year.'

The consequences are concrete. A country at 8.4% adoption today may reach 13% by 2027, while the EU27 crosses 30%. The window of opportunity for Polish-native AI tool providers will not stay open forever. When global providers refine their Polish handling (and they will), the local edge shrinks.

---

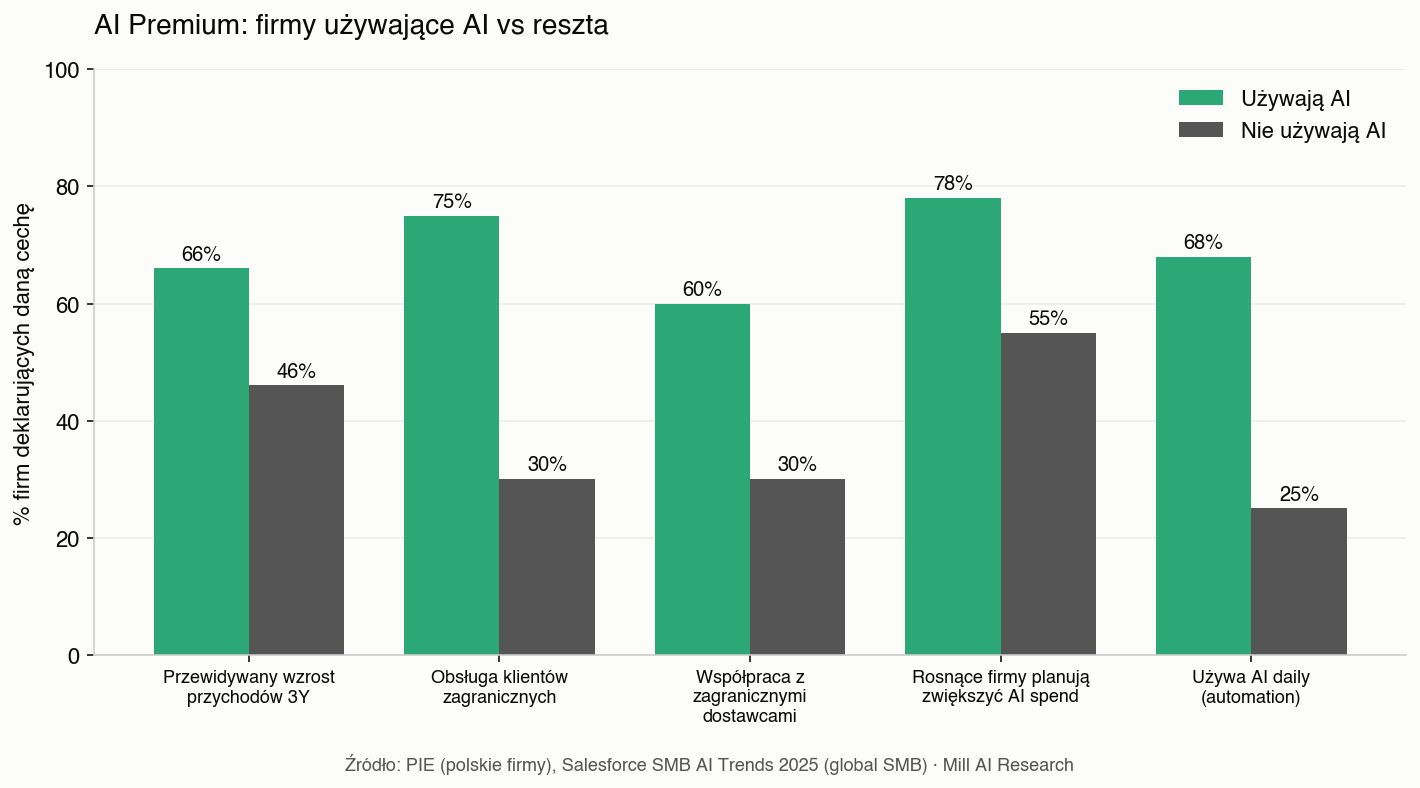

Finding 5: The AI User Premium

There is one number that should be at the center of every conversation about AI adoption in Poland, and which almost no one cites: 66% of Polish firms that use AI expect revenue growth within 3 years. That is the 2025 result from the Polish Economic Institute, 20+ percentage points higher than the expectations of firms that do not use AI.

PIE also shows other differences:

- AI-using firms are 2.5 times more likely to serve foreign clients.

- AI-using firms are 2 times more likely to collaborate with foreign suppliers.

Causality can't be inferred from the numbers alone; more internationalized firms may adopt AI more often from the start, not necessarily the reverse. Even if the relationship runs both ways, the signal is unambiguous: AI adopters are a different category of firm. More mature, more international, more optimistic about growth.

Global data from Salesforce SMB AI Trends 2025 is even more decisive. In a sample of 3,350 SMB owners across multiple countries:

- 91% of SMBs using AI report revenue growth.

- 87% say AI is helping their company scale faster.

- 86% report better margins through automation.

- 68% of SMBs use AI automation daily, up 23% quarter-over-quarter.

Among firms that are growing, 78% plan to increase AI spending in the next 12 months. Among firms that are declining, only 55%. The gap is 23 pp. AI spending is not neutrally correlated with business performance, growing firms invest aggressively, declining firms hold back, and the distance between them will deepen.

The Polish adoption premium has similar character, at smaller scale. Firms that pushed through the first five attempts with ChatGPT and learned to prompt it hold a cost and speed advantage non-adopters cannot overcome simply by growing marketing budgets. A small firm run by one person who produces a weekly content schedule for a client in an hour competes with an agency that takes two days to produce the same output, and that competition won't be won by budget.

---

Implications for Polish SMB

The Polish small-business sector operates under unusual conditions: official statistics omit it, global AI tools don't serve it in the language that is its operating language, and domestic providers largely concentrate on enterprise. At the same time, firms that have leapt these barriers and use AI report 20+ pp higher growth expectations.

What does this mean for someone running a small firm in Poland in 2026?

AI adoption is not optional today for firms operating in content, marketing, customer service, pitch writing, or document generation. It is optional only for firms that consciously accept competing on volume against competition that uses automation. The calculation works short-term, but not strategically, because performance gaps compound faster than other kinds of advantages.

Tool choice matters more than model choice. ChatGPT, Claude, and Gemini score similarly on Polish PLCC, the spread is 1.7 pp. Business outcomes are differentiated by interface, workflow, degree of automation, and specialization for a specific use case. A tool built for writing Polish e-commerce product descriptions, with templates refined for Polish context, with prompt suggestions chosen for Polish industries, will deliver better results than raw ChatGPT. Not because the model is better, but because the process is optimized.

Content is the right starting point, but not the only one. EU27 data show fast growth across all modalities: written text analysis (+4.9 pp YoY), natural language generation (+3.4 pp), image generation, speech recognition. A firm that masters content generation in 2026 can add customer-service automation in 2027, CRM-driven offer customization in 2028. That's a gradual build of operational advantage, not a one-off IT project.

Costs. Commercial off-the-shelf AI is the #1 acquisition mode in Poland in 2025, 6.4% of firms (GUS). Custom development accounts for 2.1%. The trend will hold because the economics agree: tool subscription at 30-200 PLN monthly vs. a development project at 50-200 thousand. For a small firm the choice is obvious. The question isn't 'whether to build your own' but 'which off-the-shelf to choose'.

---

Why This Matters for Europe

Poland is not just a national case. It is Europe's largest economy in the bottom quartile of AI adoption. Treating 2.76 million Polish small firms as a statistical rounding error, which is effectively what Eurostat's methodology does, creates three problems for the broader European AI agenda.

Policy blindness. European AI strategy (AI Act implementation, Digital Europe funding, Horizon programs) designs tools for the SMB segment Eurostat sees. The invisible 95.9% in Poland, and analogous segments in Romania, Bulgaria, Greece, Portugal, receive support programs calibrated to the wrong baseline.

Competitive asymmetry with the United States. In the U.S., tools for solopreneurs (Shopify, Stripe, HubSpot, Canva, Notion) are native to the small-business economy from day one because that economy is visible, measurable, and addressable. In Europe, the small-firm segment is fragmented across 24 languages and statistically underreported, which pushes European AI providers upmarket toward enterprise clients who look more like their American counterparts. The result: European solopreneurs use American tools, European enterprise uses American clouds, and European providers serve European enterprise only.

Growing inequality of adoption rates across the EU. A Denmark at 42% and a Poland at 8.4% are not members of the same AI market. They are two separate markets inside one regulatory envelope. If the trajectory continues (Denmark +14.5 pp YoY, Poland +2.5 pp YoY), by 2030 the gap will exceed 40 pp. That is not a common digital single market. That is two digital Europes.

The Polish small-business segment is the canary in this mine. If the EU wants AI adoption to be a European phenomenon and not a Northern-European phenomenon, the blind spot Eurostat built needs fixing, and the 2.76 million Polish sole proprietors need tools built for them, not translated for them.

Built by Mill AI

This report was produced by Mill AI, a platform building AI-native companies for small business. Two of our tools appear in Polish SMB AI stacks: Texts for Business (marketing copy generator) and Get Content Plan (content plans with ready-made social posts).

Raw dataset and full methodology available on request: contact@millai.eu